How Can Small Businesses Reduce Credit Card Processing Fees?

Renaissance Advisory helps businesses unlock hidden financial opportunities through Section 125 benefit programs, business funding, merchant processing, and tax credit optimization.

For small business owners, every dollar saved contributes directly to growth and sustainability. One of the most overlooked expenses that quietly eats into profits is credit card processing fees. While these charges may seem unavoidable in today’s digital payment-driven world, smart strategies can help reduce them significantly.

At Renaissance Advisory, we often remind business owners that managing operational costs—including payment processing—is just as important as exploring tax strategies like corporate tax reduction. The good news is that with a little knowledge and the right approach, small businesses can take control of processing fees and keep more of their hard-earned revenue.

In this blog, we’ll explore how credit card fees work, what impacts their cost, and practical steps you can take to reduce them.

Understanding Credit Card Processing Fees

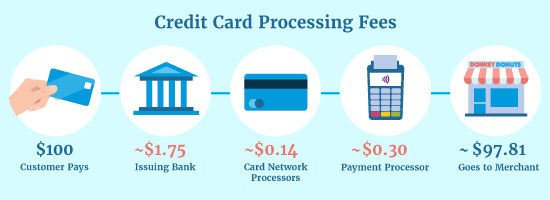

Whenever a customer pays by card, your business pays a fee to process that transaction. These fees are typically a percentage of the sale plus a flat fee per transaction. For example, a $100 purchase might result in a $2.90 fee plus $0.30, leaving you with $96.80. While that may not sound significant, multiply it across hundreds—or thousands—of transactions, and the costs add up fast.

Credit card processing fees generally fall into three categories:

Interchange Fees – Set by card networks (Visa, Mastercard, etc.), paid to issuing banks.

Assessment Fees – Charged by card networks for using their payment infrastructure.

Processor Markups – The amount your payment processor adds to cover their services.

Understanding this breakdown is the first step to reducing what you pay. While interchange and assessment fees are largely non-negotiable, the processor’s markup is where small businesses have leverage.

Why Reducing Processing Fees Matters

For many small businesses, profit margins are already tight. Every percentage point saved in processing fees goes directly toward profitability. For example, reducing fees from 3% to 2.5% on $500,000 in annual card sales saves $2,500 per year. That’s money you could reinvest into marketing, new inventory, or employee benefits.

Additionally, controlling expenses like these mirrors the broader principle behind corporate tax reduction—finding legitimate ways to minimize outflow so more money remains within the business. Just as tax strategies help retain earnings, lowering processing fees strengthens financial stability.

Practical Ways to Reduce Credit Card Processing Fees

1. Negotiate with Your Payment Processor

Many business owners accept their processor’s rates at face value without realizing they’re negotiable. Processors want your business, and if you generate steady transaction volume, you may have room to negotiate lower markups. It’s worth shopping around, comparing quotes, and leveraging competitive offers to secure better terms.

2. Understand Pricing Models

Not all processors bill the same way. The three main pricing structures are:

Flat-rate pricing – A fixed percentage + fee per transaction. Simple, but often more expensive.

Tiered pricing – Different rates depending on “qualified” or “non-qualified” transactions. Can be confusing and costly.

Interchange-plus pricing – The most transparent option, charging actual interchange fees plus a small markup.

For most small businesses, interchange-plus pricing offers the best opportunity to save.

3. Encourage Cost-Effective Payment Methods

Different payment methods carry different fees. Debit card transactions usually cost less than credit cards, and swiped/chip payments are cheaper than manually entered ones. You can:

Encourage customers to use debit cards.

Offer discounts for cash payments.

Avoid keying in card numbers unless absolutely necessary.

4. Optimize Your Merchant Category Code (MCC)

Your MCC identifies your type of business to card networks. Some industries qualify for lower interchange fees. Reviewing your MCC with your processor may reveal opportunities to reduce costs.

5. Batch Transactions Daily

Processors often impose fees if transactions aren’t settled within 24 hours. By batching and closing out transactions daily, you can avoid unnecessary charges and keep rates lower.

6. Avoid Chargebacks

Chargebacks occur when customers dispute transactions. Not only do you lose the sale, but you also pay chargeback fees. To minimize them:

Provide clear refund and return policies.

Use accurate product descriptions.

Obtain signed receipts for large purchases.

7. Leverage Technology

Modern point-of-sale (POS) systems and payment gateways often integrate advanced fraud detection, seamless batching, and optimized routing of transactions—all of which can reduce costs. While there may be upfront investment, the long-term savings usually justify the expense.

8. Regularly Audit Your Statements

Processing fees can creep up over time without notice. Review your monthly statements carefully. Look for hidden fees, rate increases, or charges for services you don’t use. If you spot discrepancies, bring them up with your processor immediately.

Balancing Cost Management with Customer Experience

While reducing fees is important, remember that customer convenience should remain a priority. Consumers today expect businesses to accept a wide variety of payment options, including credit cards, mobile wallets, and contactless payments. Eliminating certain methods to save costs may hurt sales in the long run.

Instead, think strategically:

Offer multiple payment options, but educate customers on lower-cost methods.

Be transparent if offering cash discounts.

Ensure your checkout process remains quick and seamless.

A balance between cost control and customer satisfaction is essential.

Connecting Processing Fee Reduction with Broader Financial Strategy

Lowering credit card processing fees is just one piece of the financial efficiency puzzle. For small businesses, the ultimate goal is to maximize retained earnings and fuel growth. That’s where aligning operational savings with tax strategies comes into play.

For instance, if you’re saving thousands annually on processing, those savings could be paired with a corporate tax reduction strategy to further optimize your financial position. By reducing both operational and tax-related expenses, businesses create a powerful compounding effect on profitability.

At Renaissance Advisory, we view these strategies holistically. Whether it’s helping clients uncover tax credits, reduce overhead costs, or optimize payment processing, the goal remains the same: putting more money back into your business so it can thrive.

Final Thoughts

Credit card processing fees may feel like a “cost of doing business,” but they’re far from fixed. With the right knowledge and proactive steps, small businesses can significantly cut these expenses without compromising customer experience. From negotiating with processors and choosing the right pricing model to leveraging technology and maintaining best practices, every effort adds up.

And remember, just like corporate tax reduction, this is about strategy—not shortcuts. The more intentional you are with managing expenses, the stronger your bottom line becomes.

If you’re a small business owner looking to improve your financial efficiency, consider both your payment processing structure and your tax planning strategies. At Renaissance Advisory, we help businesses uncover opportunities to save and reinvest where it matters most. After all, reducing costs isn’t just about surviving—it’s about creating room to grow.